A Veterinarian's Perspective on the Value of Pet Insurance

A Veterinarian's Perspective on the Value of Pet Insurance

One of the most common questions pet owners ask about pet insurance is: "Is pet insurance worth it?" It’s a valid question and one worth exploring.

What people usually mean by asking this question is, “Will I get more back than what I pay in premiums?”

People buy insurance of any kind to help them pay for large, unexpected, or unplanned expenses for which they would have trouble paying for out-of-pocket.

The premise of wondering if you'll get back more than what you paid in premiums over the lifetime of your pet presents a basic misunderstanding of the purpose of insurance. A better question to ask is perhaps, "Do I need pet insurance?"

If you are self-insured, that is, you have the resources (cash, savings) to pay any size veterinary bill without going into debt, you don’t need pet insurance. However, I talked to one veterinarian in an affluent area who told me that even some of his clients have pet insurance simply to protect their assets from a catastrophic pet health event.

In other words, they don’t like the idea of most of their savings being wiped out by an expensive vet bill. In this case, they would buy a pet insurance policy with a high annual maximum, higher deductible, and copay to minimize the amount they would pay in premiums but still protect them against that worst-case scenario.

I’ve also known pet owners who have told me, “If treatment is going to cost more than $500, then I’ll just euthanize him and go get another pet.” These people obviously don’t value their pet as a member of the family, and the purchase of pet insurance would indeed be a waste of money.

From my experience in practice, most pet owners don’t fit into either of these categories.

Types of Pet Healthcare Expenses

So, let’s look at the types of pet healthcare expenses that you will face during your pet’s lifetime:

Wellness care

Preventative care is annual or semi-annual examinations, vaccinations as needed, heartworm and intestinal parasite testing, heartworm preventative medication, monthly flea and tick control products, teeth cleaning, wellness blood and urine testing, spaying or neutering, etc. You likely know about how much these costs are going to be every year and when these procedures are due, so you can budget and save for them – they aren’t unexpected.

Some pet insurance companies offer wellness coverage – usually as a rider (add-on) coverage to their accident/illness policy for an additional premium.

Minor acute accidents and illnesses

Ear infections, urinary tract infections, diarrhea, insect stings, minor lacerations, etc. These problems can usually be handled as an outpatient. Even though these are unexpected events, you can usually handle these costs out of pocket.

Major acute accidents or illnesses

Any acute condition that requires surgery and /or hospitalization. In addition to being unexpected, these events are usually expensive, especially if treated at an emergency or specialty hospital. These expenses are why pet owners need a line of credit, savings reserve, and consider the purchase of pet insurance.

While some companies offer “accident only” policies for a reduced premium, I don’t recommend them unless your pet doesn’t qualify for illness coverage because of certain pre-existing conditions. The “accident/illness” policies offer much broader coverage for your pet.

Chronic conditions

Allergies, diabetes, arthritis, Addison’s disease, Cushing’s disease, kidney failure, heart failure, etc. that require treatment for the rest of the pet’s life. The mistake that most people make is assuming that chronic conditions only occur in older pets. But many start early in life – even less than a year old.

Therefore, pet owners tend to underestimate the cumulative cost of caring for a pet with one or more chronic conditions over the pet’s lifetime. About 40% of all insurance claims are for chronic conditions.

Take a look at these claims filed at Embrace pet insurance company to get an idea of the potential costs of diagnosing and treating various conditions in both dogs and cats.

I know what some of you are thinking, “Something like that would never happen to my pet.” If the only pet healthcare expenses you’ve dealt with in the past are wellness care and minor acute problems, you likely have no idea what can happen and how much it can cost, particularly if you have to go to an emergency or specialty hospital.

Dr. Barry Kipperman, owner of a 24-hour emergency/specialty hospital in California, told me that he frequently hears pet owners say, “I never imagined it would cost this much to save my pet’s life.”

Questions to Ask Yourself When Considering Pet Health Insurance

So, when deciding if you should consider purchasing pet health insurance, ask yourself these two questions:

- How much am I willing to spend to save my pet’s life if there is a reasonable chance of survival and a good quality of life after recovery? If there are other family members in the picture, this should be discussed together. I had one veterinarian tell me that a good reason to buy pet insurance is if family members disagree on the answer to this question.

- How much am I able to spend (checking, savings, and line of credit) to save my pet’s life if there is a reasonable chance of survival and a good quality of life after recovery?

If the answer to the first question is more than the answer to the second question, you should consider getting pet insurance to help bridge the gap between what you’re willing to spend and what you are able to spend if required to save your dog or cat’s life.

How Much Does Pet Insurance Cost?

Pet insurance premiums are based on:

- Species: whether your pet is a dog or cat (cat policies are less expensive)

- Age: the pet's age (higher for older pets because they are more prone to chronic diseases)

- Breed: pet's breed (some breeds are more predisposed to problems than others)

- Where you live: your zip code (veterinary care costs more in some locations than others)

Premiums will also vary according to the level of coverage you select (policy maximum, deductible, reimbursement, what’s covered or not covered). Accident-only policies are significantly less expensive than accident + illness policies.

Some pet insurance companies increase rates as your pet ages, but not all do. Premiums may also increase when a pet insurance company adjusts rates based on a review of their actuarial data – their actual claims experience versus predicted claims experience since the last time they filed rates in each state (for each breed of pet).

Listen to an interview I did with Laura Bennett, one of the Co-Founders of Embrace pet insurance, about how pet insurance companies set and increase their rates.

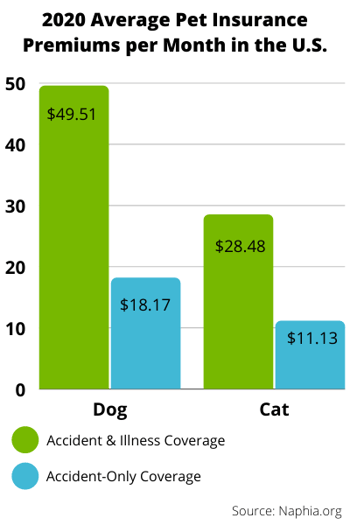

The North American Pet Health Insurance Association (NAPHIA) publishes the average rates of pet insurance in the U.S. and Canada from their participating insurance company members. Monthly policy premiums can be much higher than these averages, especially for older pets, as well as breeds that are predisposed to illness. Premiums can be as high as $200 a month or more.

Premiums for cats are roughly half the premiums for dogs. Statistics show that of all the pets insured in the U.S., about 80–85% are dogs, and only 15–20% are cats. So, cat owners need to know that it is very affordable to insure their cat – even older cats.

How to Customize Your Pet Insurance Premium

Most pet insurance companies allow you to customize your policy by selecting among several different annual maximums, deductibles, and copays. Some allow you to further customize by making some coverages optional, e.g., exam fees or alternative therapy (rehabilitation, acupuncture, laser therapy, hydrotherapy, etc.), or wellness care.

Here are some general guidelines you can apply when designing a policy that will fit your budget and limit your out-of-pocket costs, especially when faced with a large insurance claim:

- Annual Maximum: Choose a policy with the highest annual maximum that you can afford. You buy pet insurance for help with large bills that you would have trouble paying for out-of-pocket. Ask yourself, "What if I had a bill that was $10,000 or even higher?” Some companies have policies with no upper limits (no lifetime, annual, or per-incident limits).

- Deductible: Choose a policy with the lowest deductible you can afford. Deductibles are either annual or per condition/accident. Deductibles will usually vary from $0 to $1,000.

The annual deductible is more predictable because once it’s met during a policy year, you’ll only have to pay the copay (and any uncovered items) when filing a claim.

If a company has a per-condition deductible, be sure to clarify how it works. Usually, once a deductible is met for a condition, you won’t have to pay another deductible for that condition for the rest of the pet’s life (great for chronic conditions). But for each new acute condition, you’ll have to pay a deductible. - Copay: Choose a policy with the lowest copay you can afford (highest reimbursement). Copays usually range from 0% to 50%. Unless you selected a 0% copay when customizing your policy, you'll pay a copay with every claim. So, you’ll want to keep this as low as possible.

Make Your Pet Insurance Policy Fit Your Budget

When trying to lower a premium so that it fits your budget, here's my recommended priority:

- First: Select a higher deductible. This will have the most impact on the premium.

- Second: Increase your copay (lower the reimbursement you will receive).

- Lastly: You can lower your annual maximum. In my opinion, this should be changed as a last resort because you want your policy to cover a worst-case scenario above all else, and it usually has the least impact on the premium. Not all insurance companies provide the option to lower the annual maximum.

If you are in a financial position to pay more out of pocket, consider a higher deductible and lower reimbursement to significantly lower the premium. This way, you're paying less monthly and only paying more in the event your pet needs accident or illness care.

Choose the Best Coverage You Can Afford at the Beginning

An important reason for getting the best coverage you can afford when you first sign up for pet insurance is because premiums will likely rise over time. There are a few reasons for this: 1) due to inflation, 2) possibly because your pet is getting older, or 3) when the company makes rate adjustments based on their actuarial data.

If the premium gets out of your comfort zone, you can downgrade the coverage (drop optional coverages you don't need anymore, raise your deductible or copay, or decrease your annual maximum) to lower the premium. Most companies will allow you to do this without penalty.

However, if you want or need to upgrade the coverage (lower the deductible or copay or raise the annual maximum), your pet may be subject to underwriting again, and any conditions that were previously diagnosed/treated (even while insured) will likely be considered pre-existing and not covered after the upgrade.

How to Choose the Best Pet Insurance Company and Policy for You and Your Pet

I’m going to share with you the most important things that should be covered in a pet insurance policy from my perspective as a veterinarian. After all, I spent many years diagnosing and treating the accidents and illnesses that you will end up filing claims for.

Also, after writing and podcasting about the pet insurance industry for over a decade, I’ll share with you some additional factors you need to consider before purchasing pet insurance. I believe if you take my advice, you’re much more likely to make a wise decision with fewer regrets when choosing a company to insure your pet.

What Should Be Covered in a Pet Insurance Policy?

Exam fees

Some companies don’t cover exam fees, and others make it optional. Other companies include it automatically in their policy. If it’s not covered, it’s like paying an extra copay every visit. This could get expensive if your pet has a problem that requires multiple rechecks, you visit an emergency or specialty hospital, or you’re one of those people who take your pet to the vet at the first sign of anything abnormal.

Alternative and Rehabilitative Therapy

Veterinarians are prescribing these therapies more and more, especially after orthopedic surgery or injuries. Be sure to find out what a company includes in such coverage. Look for treatments like laser therapy, hydrotherapy, and acupuncture. If a company makes this coverage optional, you’ll usually be able to add it when you get a quote.

Prescription Foods

Therapeutic diets are usually prescribed to help manage chronic conditions like arthritis, allergies, diabetes, urinary disorders, etc. These foods generally cost about twice as much as the food a pet usually eats. I had clients whose pets would have benefited from these diets, but they simply couldn’t afford the costs long-term. Even if a company covered 50% of the costs of prescription food, that could make it affordable for more people. Ask if there are limits on this coverage.

Dental Illnesses

Pet insurance companies will not cover the expense of dental cleaning, which is a preventive measure, but they should cover expenses associated with dental accidents, like a fractured tooth from trauma (e.g., cracking it on a hard chew toy). Since most of the dental problems seen by vets are due to dental illnesses — periodontal disease, oral tumors, feline gingivitis/stomatitis, and feline tooth resorption — check the policy to make sure these types of dental issues are covered. Also, ask if the policy covers root canals and crowns on what are considered vital teeth, like canine teeth and fourth upper premolars (also known as the carnassial tooth). And ask if there are special limits on these coverages.

Congenital and Hereditary Conditions

These are conditions that a pet is born with or inherits from their parents' lineage. Virtually all the companies cover these now, but some companies put age limits and may require a longer waiting period before coverage begins, so be sure to ask about this.

Behavior Problems

Behavioral issues or concerns like separation anxiety, noise phobias, litter box aversion, etc., are treatable or at least manageable with the appropriate care. Behavior issues are the #1 reason pets are surrendered to shelters or euthanized every year. These issues are better prevented than treated, but these problems can require multiple vet visits and long-term therapy and management – possibly even referral to a specialist. Ask if there are any limits on coverage.

Supplements

Supplementation, especially for orthopedic conditions, liver disorders, etc., can be very helpful. The ones that are usually effective and have scientific and anecdotal evidence that they actually work are more expensive than over-the-counter (OTC) alternatives. Since they may be needed long-term, they can be costly.

Other Factors to Consider. Questions to Ask a Pet Insurance Company.

What are the waiting periods?

This is the length of time after sign-up until coverage actually begins. Any problem the pet had before sign-up, or that occurs during the waiting period, will be considered pre-existing and not covered. This will vary from a couple of days for accident coverage and 14–30 days for illness coverage. Obviously, shorter is better.

Some pet insurance companies will waive the waiting period for illnesses if you sign up within one day of a veterinary exam. Any problems found during that exam may be considered pre-existing and, therefore, not be covered.

Will the insurance company pay the veterinarian directly?

If the vet agrees to accept payment from the insurance company, will the insurance company pay them directly? This is particularly helpful in the case of a large claim where you can’t come up with the full amount of the bill and wait for reimbursement.

If you aren’t able to pay any veterinary bill out-of-pocket with a debit or credit card, this is an important option to have available if needed.

Will the insurance company pre-approve (certify) a claim?

For potentially large claims, the pet parent may want to know if it is going to be covered before giving the go-ahead for treatment or surgery. If the veterinarian agrees to accept payment directly from the insurance company, they will also want to make sure it is a covered expense.

Only one company (Trupanion) is currently capable of doing this 24/7 within minutes. This is how pre-approvals should work. Other companies may pre-approve a claim, but the process may take days to determine. Unfortunately, this is only helpful for non-urgent problems.

Will the company do a medical record (history) review?

Immediately after the waiting period, will they review your pet's medical history to determine if there are any pre-existing conditions that won’t be covered? Will they let you know in writing the results of the review? This goes to the heart of transparency.

The #1 reason for negative reviews of pet insurance companies, by far, is claim denial because of a pre-existing condition. Therefore, if your pet has been diagnosed or treated for one or more problems in the past, you need to buy a policy from a company that does this automatically upon sign-up or when requested.

Most companies will only ask for and review your pet’s medical record after a claim is filed. In my opinion, you deserve to know up front if there are pre-existing conditions. I’ve read many reviews where a pet parent had paid premiums for several years before filing a claim, only to have the claim unexpectedly denied because the condition was considered pre-existing. Needless to say, they weren’t happy.

Will the company cancel your policy, raise your premiums, or downgrade your coverage based on how much you claim in a given year or the lifetime of your pet?

The most common reasons a company will cancel your policy are for non-payment of premiums or if you gave fraudulent information about you or your pet when you signed up or during the policy term.

Sometimes companies will come out with a completely new policy, and if your pet is eligible for coverage with the new policy, your old policy will be canceled. Your pet will then be enrolled and covered with the new policy. The coverage and premium will likely be different with the new policy. If this happens, make sure conditions that were covered under the old policy will still be covered under the new policy.

How to Find a Company to Insure Your Pet

With 20+ brands of pet insurance now, it can be overwhelming to pick one for your pet. I think the problem most people have is trying to compare all these companies with each other.

A better approach is to compare each company individually with your specific needs and priorities. Pet insurance isn’t one-size-fits-all. There’s no best company for everybody.

Your financial situation and budget are unique. Your pet’s medical history is unique. What’s best for someone else may not be best for you. Therefore, the first step will be considering the coverages I mentioned above. Which ones resonated with you? Of the other factors mentioned above, which ones are most applicable to your needs? Focus on these.

The next step is getting a quote from the companies that offer the broadest coverage. In light of the premium, consider what each company’s policy covers and doesn’t cover and how they stand on the other factors that are important to you. A lot of this information is available on their website (even their quote page).

If you are having trouble finding information, consider using their chat feature or call the company to get all of your questions answered. This will allow you to eliminate those companies whose premiums are simply out of your comfort zone or that don’t fit the specific needs of you and your pet.

Now it’s time to read a sample policy of the handful of companies that remain. Read every word. Here you’ll find out information that isn’t available on their website. If there is anything you don’t fully understand, call and talk with a company representative to get clarification.

Of the 2 or 3 companies that remain, you may want to read some reviews from several review websites before making your final choice. Read both positive and negative reviews. One reason I don’t prioritize reviews is that review websites are generally susceptible to manipulation and, therefore, can be misleading.

Only then is it time to compare companies with each other and make your final choice.

In my opinion, and based on feedback I’ve gotten from numerous pet parents with regrets about the company they chose to insure their pet, you’ll need to invest some time to do the research needed to make a wise decision.

The temptation is to just simply go with the company your veterinarian or your friend recommended. Or, perhaps the company you work for is offering pet insurance with a certain company as an employee benefit. Before buying pet insurance from a company someone else recommended, you owe it to yourself and your pet to evaluate that company based on the factors above that matter the most to you.

Choosing wisely is important because if you eventually decide to switch companies, conditions your pet was covered for under the old policy will likely be considered pre-existing and not covered under the policy of the new company.

I offer a Pet Insurance Toolkit for pet owners who are interested in doing their own research. Many pet parents over the years have told me it was very helpful in guiding them through the research process. Information about alternatives to pet insurance is included in the toolkit.

I also host a podcast dedicated to pet insurance that has a wealth of information not available anywhere else. I’ve interviewed representatives of most of the pet insurance companies in the U.S. – oftentimes the Founder/CEO of the company. In my opinion, these interviews are perhaps where you’ll find the most valuable information about each company.

I also interviewed Anne Tomsic, the founder of Preventive Vet, on my podcast. She has insured all of her dogs for the last 20 years. Her experience and advice for pet parents are worth a listen. Listen to the episode out here.

I believe that more and more pet owners will purchase pet insurance in the future because technology and the costs of delivering quality healthcare to pets have outpaced the ability of many pet owners to pay for emergency and unexpected care. While pet owners and veterinarians can potentially benefit from medical insurance to help pay for the healthcare of pets, I'm convinced the real winners will be the pets.

What Should You Do If You Don't Buy Pet Insurance?

The best thing you can do to minimize your out-of-pocket expenses for your pet’s healthcare is to prevent problems that require unexpected visits to the veterinarian. Prevention not only saves you money but saves your pet from unnecessary pain and suffering and may even save your pet’s life.

There is no better resource for information on prevention than this Preventive Vet website, and especially their books, written by Dr. Jason Nicholas. To learn just how valuable I consider this information, listen to this podcast interview I did with Dr. Nicholas about these 101 Essential Tips books.

The next best thing you can do is to just have a plan in place to pay for your pet’s healthcare. I’ve written a short ebook, “How To Pay For Your Pet’s Healthcare,” that I believe will be a valuable resource in helping you design a plan that works for you. This also includes information about alternatives to pet insurance. Information about how to obtain the book is available on my blog.